What is Profitability?

“The bottom line is that we have to earn a profit to stay in business!” Family business owners fully understand the gravity of this truth. But what is profit? At its roots, profit is simply the state or condition of yielding a financial gain in an enterprising activity after all of the expenses are paid.

In a family business, profit is much more. It is the fuel for growth and the necessary ingredient for liquidity. It is also intensely personal, as profit may be the source of a year-end bonus for an executive, a new machine for the production team, or payment for a daughter’s education when distributed to a shareholder. In fact, profit is so personal that our very relationship to money impacts how we view profit.

For those who deeply value the prestige and power gained from wealth, there may be an intense drive to maximize profit so that large distributions can be made to support growing lifestyle demands and interests. For those who value work-life balance, there may be a desire to provide flexible schedules and support resources to company employees, even if it means less profit at the end of the year. Even the work culture can impact how various stakeholders view profit. For example, when open book management is successfully implemented, every employee from top to bottom asks prior to a spending decision: “How much will this increase or reduce profitability?”

In a family business, profit is not a black-and-white concept. It is seen as a dynamic mix of business performance, stakeholder personality, and family business culture.

How do Different Stakeholders View Profitability?

In order to understand the dynamics, we need to look at how different family business stakeholders commonly view profitability:

Owners

Owners often see profit as the fuel to reach their ownership vision and mission, which varies from owner to owner. Owners see profit as key to ownership continuity. They wish to receive long-term returns on investment and access to liquidity when ready to harvest their ownership returns. They may also seek shorter term liquidity in the form of dividends or distributions. Lack of profit may be personally threatening when bank loans and guarantees are present.

Managers

Employees often see profit as the key to accessing new work tools (better computer, new machine, improved lighting or additional staff) and also improved lifestyle and wealth building (salary raises, bonuses, new benefits or time off). Too often their view is disconnected from the concept of owner’s need for return on investment, especially if not given enough information.

Board of Directors

Directors often see profit as a key measure of the CEO’s success in executing the strategic plan. They are concerned about being within limits of bank covenants. Directors need to understand the owner’s views on profitability in order to represent them in the board room. Independent directors understand management’s desires to benefit from greater profitability, as they have served as executives. The board needs to become more involved in corporate decision making if management does not generate profit in line with expectations.

Family Members

Family members want predictability from the business: to know what can be expected in terms of profit use for dividends or distributions. They may perceive lack of sharing profits as being controlling and related to their family status. Parents who control ownership may fear too much profit being used as dividends to younger adult stockholders. Family members may judge other family members by how distributions from profit are used.

In pass-through entities such as S-Corps and LLCs, shareholders are often perplexed as to how taxes work related to profit. With lack of accurate knowledge, they may feel threatened (How can I pay for this giant tax bill?) or even manipulated (What are they not telling me?). Family members may struggle with having income from outside the family business taxed at a higher rate due to the family business income being high, and question the value of family business ownership if distributions are minimal.

Suppliers

Suppliers want assurances that the company is making a profit to be able to pay for supplies. Suppliers may impose more difficult terms if they perceive profitability challenges. Additionally, supplier credibility can lead to opportunities such as expanded product line availability.

Customers

Customers want a quality product at a cheap price. They may feel taken advantage of if they perceive the company has made too much money off of them. When the customer is a larger company, the customer may require open sharing of financial information and place limits on the level of profit that the family business is allowed to make. The customer may also want assurances of long-term viability to supply the product in a sustainable manner.

Banks

Banks are willing to loan money when they know they will get paid back. They set a profit threshold that must be met in the form of bank covenants. Banks may require an external work out team if profitability requirements are not being met.

How do We Measure Profitability in a Family Firm?

A critical part of achieving stakeholder understanding and alignment on profitability goals is to measure it in such a way that fosters stakeholder comprehension and acceptance. The foundational measurement of profitability is fairly straightforward: revenue minus expense = profit. However, measuring profit in a family business has a few nuances that must be addressed in order for it to be considered by stakeholders as a reliable measuring stick useful to ownership and management decision making.

The nuances of profitability measurement relate to three fundamental expenses:

- Family employee compensation and benefits;

- Related party transactions with other family owned entities and with family members; and

- Philanthropic expenditures that may be made by the business.

When there is a lack of alignment on which expenses to measure, it may negatively impact the alignment on the measurement of profit. To navigate these nuances, it is helpful to have policies that manage expectations of profitability within the family – but only if these policies are applied consistently. Such policies may include a family member compensation policy for salary, variable pay, benefits, and perks; a related party transaction policy; and a philanthropic expenditure policy.

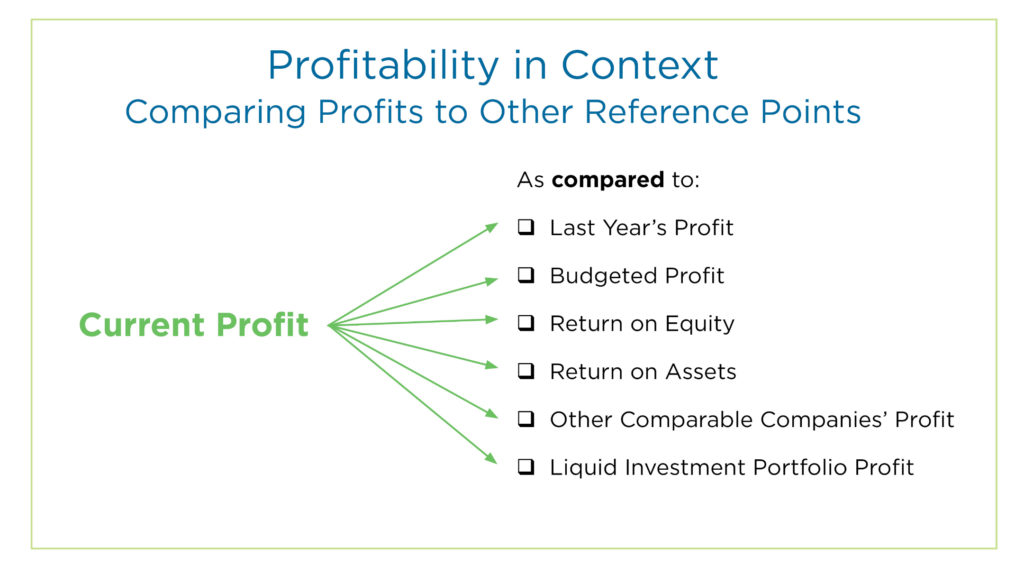

However, profit measurement alone does not provide sufficient meaning for decision making within a family firm. Putting profit into context gives it greater meaning and makes it a useful tool for stakeholder dialogue and decision making. Comparing the amount of profit to another reference point gives it meaning, such as this year’s profit compared to last year’s; actual profit as compared to budgeted profit; profit as compared to owner equity (return on equity); profit as compared to revenue (profit margin); or profit as compared to assets (return on assets). Each family business should establish the best way to put their profit measurement into context and rely on well-accepted comparisons.

To add depth to this dialogue, compare your family business’s profit to equivalent businesses in your industry over time. Determine if you are performing on, above or below par with your peers and see how you measure up. This takes into consideration industry-wide economics and the impact of economic tailwinds and headwinds on your family business’s financial performance. Another useful assessment is to compare a firm’s profit in relation to liquid investment portfolio profits.

Why is Measuring Profitability Important?

There are several reasons why measuring profitability is important. First, the understanding which arises from the types of comparison builds context for stakeholders. This context can provide an objective foundation for the ownership group to support the management team in the face of difficult economic conditions. It can also challenge the board of directors and management team if the business is performing below par. Second, without this objective analysis and its use in the dialogue around the business’s performance, family stakeholders are left to make assumptions that often turn out to negatively impact their viewpoint. This can lead to unnecessarily subjective conclusions and make already difficult conversations even more challenging. Finally, objective analysis and open dialogue help family stakeholders better understand which levers can be used to increase and decrease profits as well as provides a platform for good decision making.

How do Families Create Good Decision Making Processes Related to Profitability?

Given the wide-ranging perspectives that operate in a family enterprise, it is not surprising that profitability can create tension and conflict within business-owning families. So who in the family enterprise system gets to decide on the profitability goals for the business? And how do we create good decision and alignment regarding profitability within business owning families?

We suggest that the decisions related to profitability primarily rest with the company’s shareholders because they own the business as well as assume and manage all related risks. This ownership entitles them to make decisions in the domain of profitability, exercised through the board of directors. However, setting profitability goals should not be done in a vacuum. Management’s voice is critical to understanding what the business is capable of doing, and gaining alignment between ownership and management on goals to pursue is critically important to its success. It may also be wise to seek family input and alignment on profitability goals when an open communication forum has been established.

Making profitability a normal part of discussions among family members is an important aspect of creating healthy decision making around this matter. Below is an example of a big picture discussion that family stakeholders might engage in around profitability decision making:

Profitability Decision Making Worksheet Download example and blank worksheet

Some important steps to help foster a frank and open discussion around profitability within the family business include:

- Utilize a family values exercise to illuminate each person’s relationship to money and to move the topic of money/profitability from being an undiscussable in your family to being one that can be more comfortably talked about. It provides opportunity for individuals to share their expectations and desires around money and profitability without judgement.

- Develop a family vision and values statement with the family to help the owners (should they be a subset of the family) set an overall direction and profitability goals for the company. The company’s management would then build a strategy designed to achieve the owner’s goals and the family’s vision and values.

- Implement a learning plan that builds the knowledge and skill of all family members to understand the financial elements that are material to being a responsible owner of a family enterprise including philanthropy.

- Provide regular forums (e.g., quarterly meetings) to review and discuss the financial picture of the business and other matters related to money. These discussions offer an opportunity to enhance transparency around money and profitability, reduce the power of any related undercurrents, and build understanding and synergy amongst family owners regarding profitability. Being transparent and sharing information about the current financial status of the business fosters knowledge about how well or not things are going in the business and therefore a greater ability to contribute to profitability discussions.

- Create key policies that relate to profitability and money for your family enterprise, such as:

- Employment compensation (for those working in the business full or part time including salary, variable pay, benefits and perks)

- Project compensation (for special projects completed by owners or family)

- Non-family employee compensation (sharing the pot with other key stakeholders)

- Dividends/Distributions to owners

- Related party transactions (including vendors and suppliers and actual or guaranteed loans)

- Charitable giving (expectations of giving back to community, region or globe) and related expenditures

Conclusions

Mixing family and money in business can be confidently accomplished when families take the time to educate themselves on the concepts and key issues surrounding profitability, build forums to gain alignment on their goals, and set policies to clarify expectations on profitability related matters. While this requires investment by business owners to accomplish and may include challenging discussions among the owning family, the clarity and alignment offered can result in a great return on the investment.

March 10, 2016